Recently, you’ve probably seen headlines like:

- “Loan rates are rising”

- “Interest burden is becoming unbearable”

- “Cash flow is being drained by debt”

For those who bought assets using leverage during low-interest periods,

the current environment feels very different.

This is not just a personal issue.

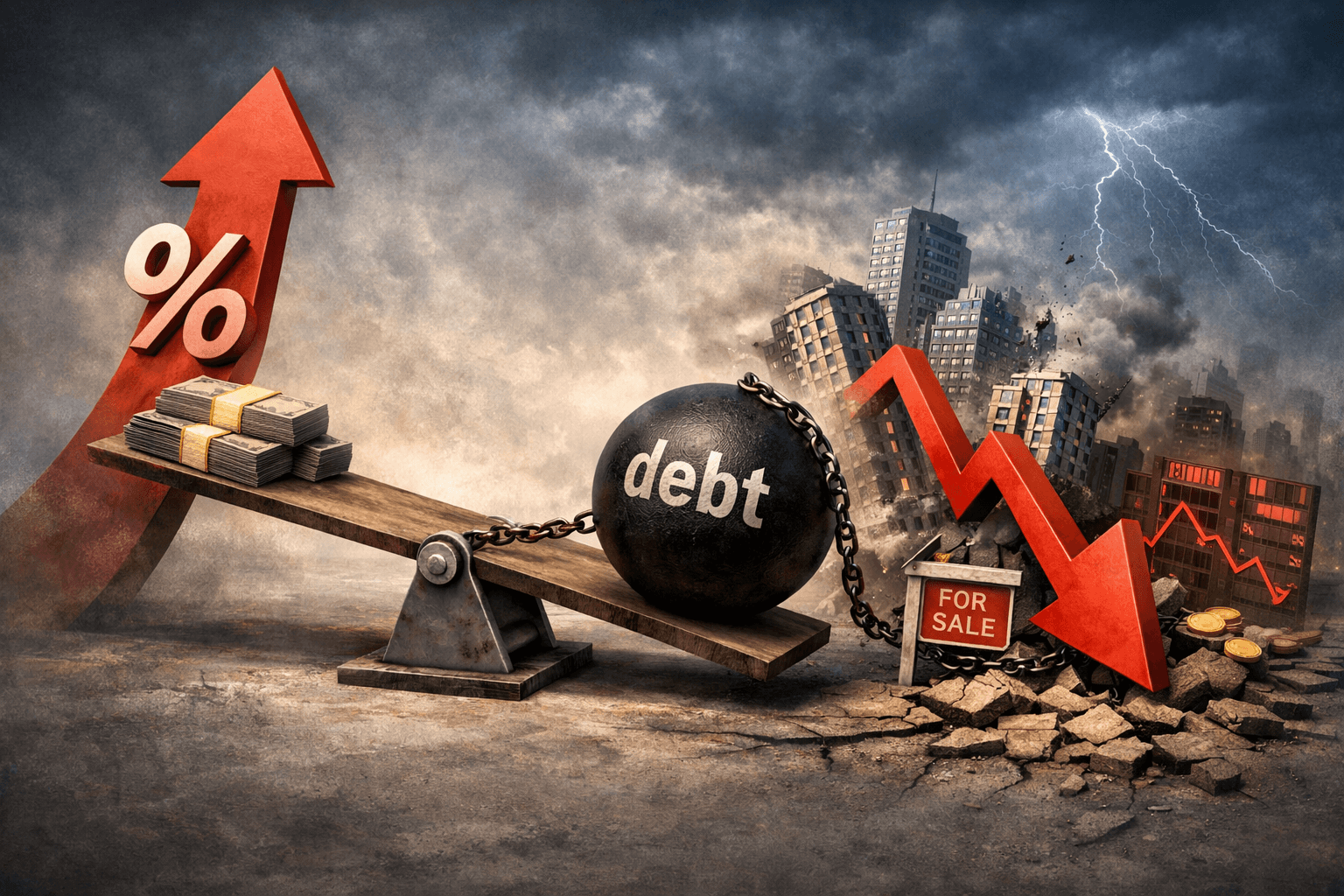

👉 It is a structural chain:

Interest rates ↑ → Leverage pressure ↑ → Asset prices ↓

In this article, we break down

why rising interest rates destabilize real estate

and how this spreads across the entire market.

1️⃣ Rising Rates Increase Interest Costs First

When interest rates rise,

the first impact is on borrowing costs.

Example:

- Loan rate at 2% → manageable

- Loan rate at 5% → significantly higher burden

Even with the same asset,

monthly cash outflows change dramatically.

At this stage:

👉 asset prices may still hold

👉 but cash flow begins to weaken

👉 Related reading: Why Interest Rates Move All Assets — The Most Important Investment Factor

2️⃣ Leverage Amplifies Everything

Leverage magnifies both returns and risks.

When rates are low:

- you can control large assets with small capital

- gains are amplified in rising markets

But when rates rise:

- interest burden increases

- profitability deteriorates

The same structure works in reverse.

At first, leverage feels efficient:

👉 “Low rates + rising assets = easy gains”

But when the environment shifts:

👉 the key question becomes not profit,

👉 but how long you can hold the asset

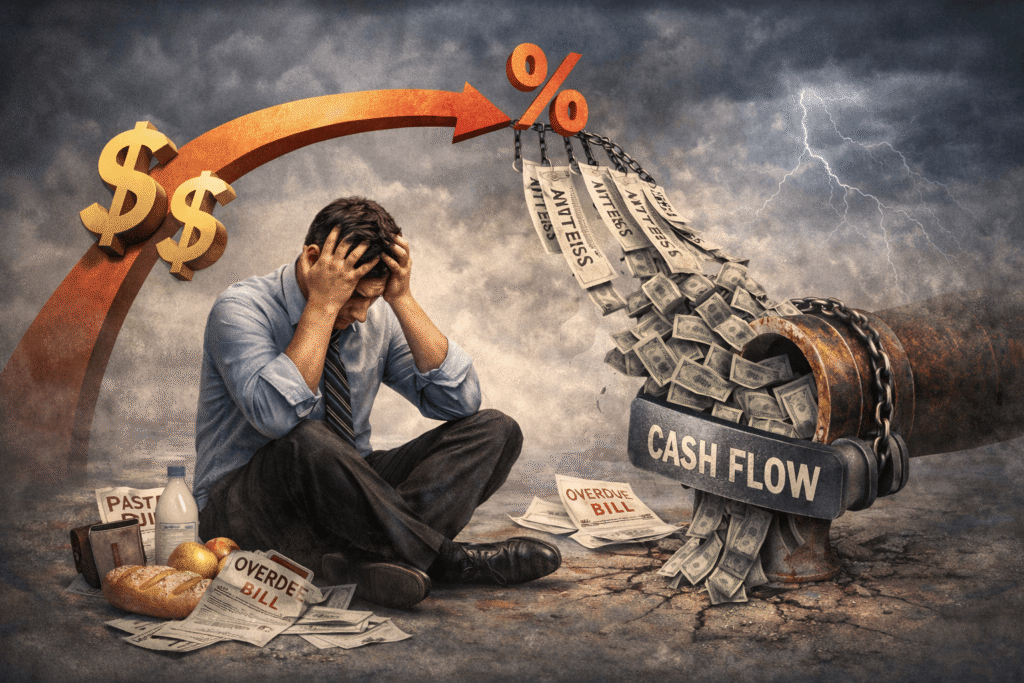

3️⃣ The Real Problem Is Cash Flow

In the end, everything comes down to cash flow.

When rates are low:

- interest feels manageable

- rising asset prices mask the burden

So people think:

👉 “This level of debt is fine”

But when rates rise:

- interest payments increase

- monthly outflows become visible

At this point:

👉 it is no longer an investment issue

👉 it becomes a lifestyle pressure

4️⃣ When You Can’t Hold, You Are Forced to Sell

The process evolves like this:

👉 Interest rates ↑

👉 Interest payments ↑

👉 Cash outflow ↑

When income cannot cover the burden:

- savings stop

- spending is reduced

- survival mode begins

At this point,

choices disappear.

Originally:

👉 “Hold or sell” was a decision

Now:

👉 it becomes a forced situation

- inject more capital

- or sell the asset

This is not a strategic sale.

👉 It is a forced liquidation

👉 Related reading: How Leverage Works — Why It Can Double Both Gains and Losses

5️⃣ Forced Selling Pushes the Entire Market Down

When forced selling increases,

a personal issue becomes a market-wide problem.

- supply increases

- demand weakens

- prices fall

This cycle reinforces itself.

👉 Interest rate ↑

👉 Individual pressure ↑

👉 Market decline

This is how a real estate downturn spreads.

👉 Related reading: Oil at $150 — What Happens to Inflation, Interest Rates, and Markets?

📌 Final Thoughts

Real estate does not fall simply because rates rise.

The core issue is:

👉 leverage structure

- Interest rates = price of money

- Leverage = amplification system

- Cash flow = survival condition

When these interact,

markets either rise or collapse.

In investing, the real question is not:

👉 “How much can I earn?”

But:

👉 “How long can I survive?”