Once you decide which ETF to invest in,

the next question naturally comes up:

👉 Should you invest all at once?

👉 Or invest gradually over time?

This is not just a difference in method.

It directly affects:

- returns

- risk

- emotional stability

So instead of asking which one is better,

this article focuses on:

👉 Which strategy fits which situation

1️⃣ The Core Difference Between the Two Strategies

Let’s simplify it first.

✔ Dollar-Cost Averaging (DCA)

- Invest a fixed amount regularly

- Example: investing every month

👉 “Spreading investment over time”

✔ Lump-Sum Investing

- Invest all available capital at once

👉 “Concentrating on timing”

So structurally:

- DCA → reduces timing risk

- Lump sum → maximizes market exposure

👉 DCA = risk distribution

👉 Lump sum = full exposure

👉 Related reading: How to Start Investing in Global ETFs — A Beginner Portfolio Guide

2️⃣ Which One Has Higher Returns?

Historically,

lump-sum investing often produces higher returns.

Why?

Because markets tend to rise over time.

👉 The earlier you invest,

👉 the longer your money stays in the market.

But there’s a critical condition:

👉 Timing matters

If you invest a large amount near a market peak:

- you may experience significant short-term losses

- recovery may take time

On the other hand, DCA:

- buys less when prices are high

- buys more when prices are low

This naturally smooths out volatility.

👉 Lump sum → higher potential return

👉 DCA → lower risk and smoother experience

👉 Related reading: Why Portfolio Rebalancing Matters — When, How Much, and What to Adjust

3️⃣ When DCA Is the Better Choice

DCA is more suitable if:

- you are a beginner

- you feel uncertain about timing

- you invest using monthly income

- you want to reduce emotional stress

A key advantage:

👉 psychological stability

Instead of asking:

- “Is this the right time?”

You follow a simple rule:

👉 “I invest consistently.”

This reduces hesitation

and prevents missed opportunities.

DCA works best when:

- income is regular

- market direction is unclear

- consistency matters more than precision

👉 DCA = sustainable investing structure

👉 Related reading: How Should You Split ETFs in an Uncertain Market? — An ETF Strategy Based on “Roles,” Not Products

4️⃣ When Lump-Sum Investing Makes More Sense

Lump-sum investing becomes powerful

under certain conditions.

It works best when:

- markets have already declined significantly

- long-term upward trend is expected

- you have a large amount of capital

- you can stay invested for a long time

Why?

Because markets often rise quickly

in short bursts.

If your capital is not invested during that period,

you may miss a large part of the gains.

Important clarification:

👉 Lump sum is NOT about perfect timing

It is about:

👉 staying invested during favorable conditions

The goal is not:

- to catch the exact bottom

But:

- to enter at a reasonable level

- and remain invested long enough

👉 Lump sum = time in the market advantage

👉 Related reading: What Happens When Cash Allocation Increases? The Beginning of Portfolio Stability and Capital Flow Changes

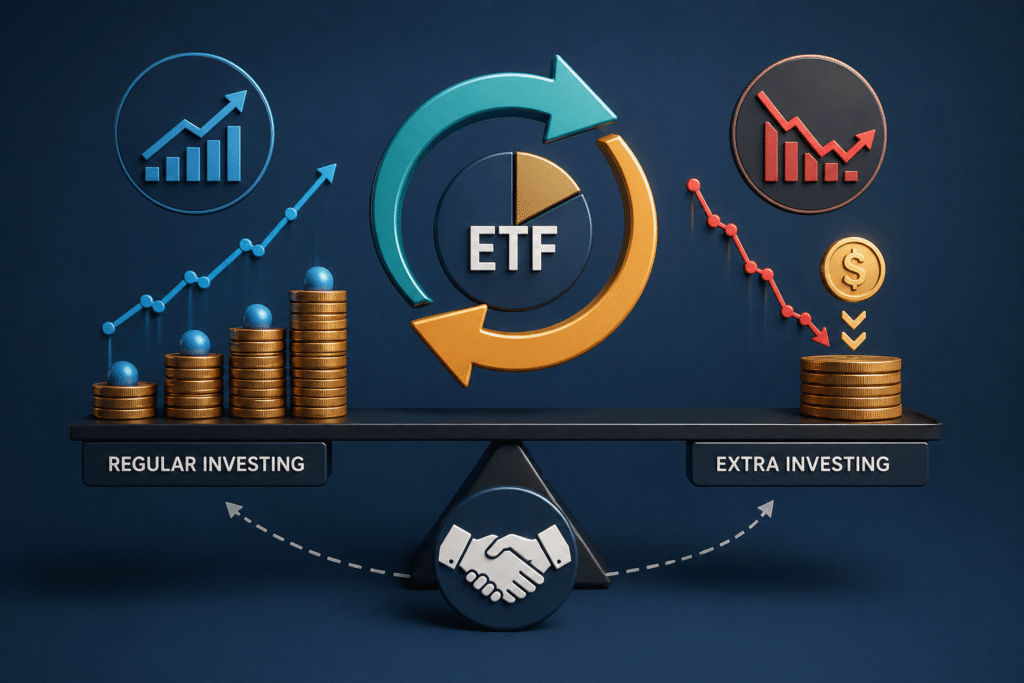

5️⃣ The Most Practical Strategy — Combine Both

In reality,

the best approach is often a combination.

A practical structure:

- invest regularly (DCA)

- add extra investment during market declines

This allows you to:

- benefit from long-term growth

- take advantage of downturn opportunities

- reduce timing pressure

Example:

- monthly DCA → consistent exposure

- market dip → additional lump-sum investment

👉 DCA + opportunistic lump sum = balanced strategy

📌 Final Thoughts

Dollar-cost averaging and lump-sum investing

are not competing strategies.

They serve different purposes.

- DCA → stability and consistency

- Lump sum → efficiency and growth

The best strategy is not choosing one.

👉 It is knowing when to use each.

Investing is not about finding a perfect answer.

👉 It’s about building a structure that fits your situation.

1 thought on “Dollar-Cost Averaging vs Lump-Sum Investing — Returns vs Risk Explained”

Comments are closed.